An ACH payment is a bank term that stands for Automated Clearing House. ACH payments are electronic transfer systems that move money between bank accounts in the U.S. A few examples of ACH payments include direct deposits, payroll, online bill payments, tax refunds, and vendor payments for merchants and small businesses.

Automated Clearing House Network

Since 1974, the Automated Clearing House (ACH) Network has been run by the National Automated Clearing House Association (also known as NACHA). In other words, they are responsible for the majority of all payments in America.

The ACH Network that is responsible for the payments is one of the biggest payment networks in the U.S. In 2018, nearly 23 billion transactions were processed valued at more than $51 trillion. According to one source, the number of transactions in 2017 was equal to approximately 66 transactions and more than $140,000 for every living American. The ACH payment network also represents more than 10,000 financial institutions, not to mention consumers and businesses.

Pretend for a moment that you’re a business owner with a utility bill to pay. You had previously provided your account and bank routing number to the utility company and approved direct bill payments. The company sets up an ACH debit to pull money from your account.

ACH Credit: Pushing money

Assuming that you are still that same owner with a utility bill, you can also initiate the payment. You can create an ACH credit to withdraw or push funds from your account to the utility company.

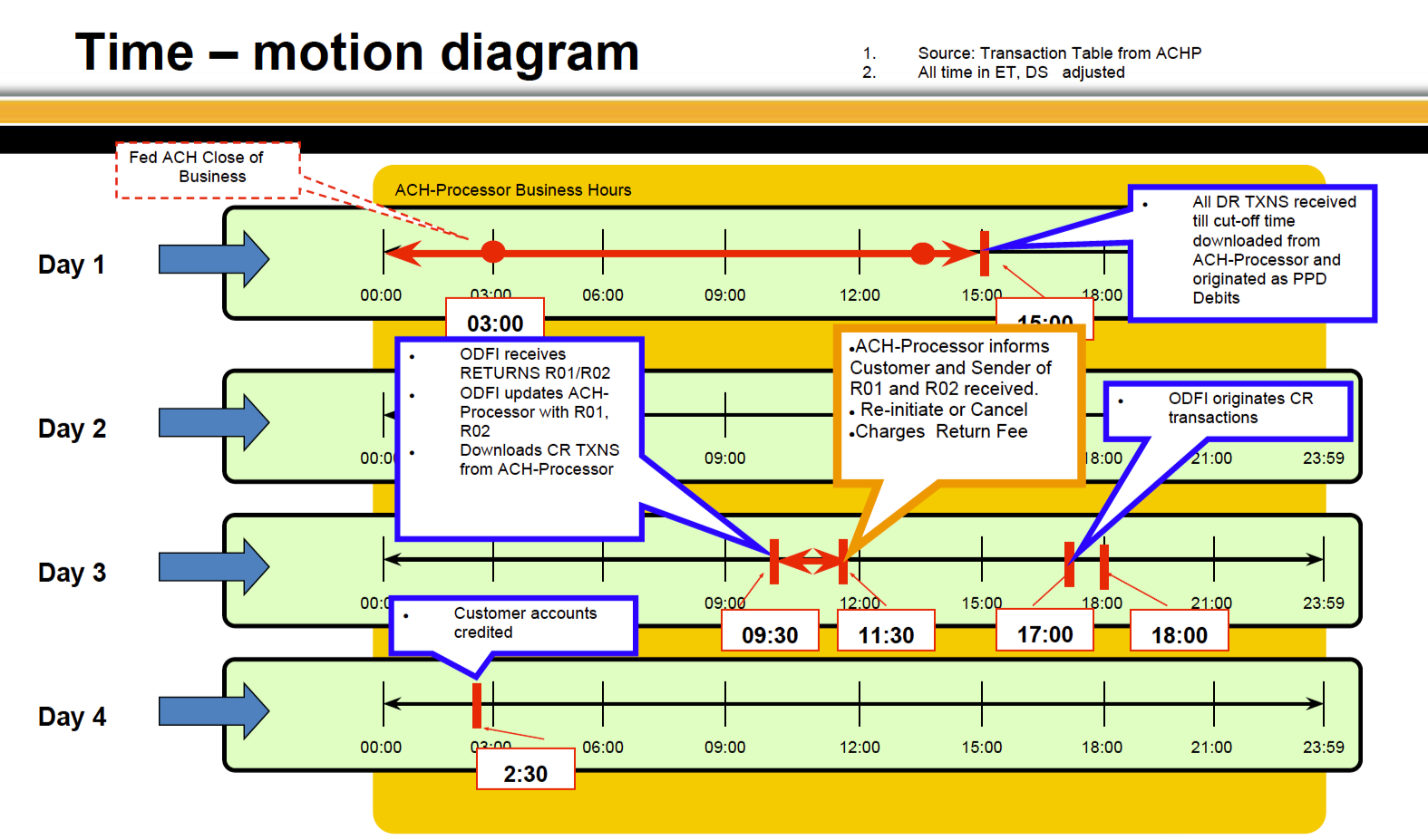

Processing ACH Payment Transactions

In order to receive or send ACH payments, one has to connect their bank account and routing number to enable automatic payments online. Once that’s happened, here’s how the processing works:

Initiate transfer: Sending money triggers an initial transfer request to the central clearinghouse.

Sorting: The ACH Network sorts the payment requests and sends it to a receiving bank.

Processing: This bank processes the transfer to either an ACH credit or debit. If the payment is approved and was an ACH credit that “pushed” funds, the transfer is complete.

Pulling funds: If “pulling” funds, or an ACH debit, then the funds must move back through the clearinghouse before arriving in the other account.

How Long Does An ACH Transfer Take?

The ACH Network processing time is getting faster and easier with every innovation but can still take up to 3-5 business days. This is because of the multi-step process and various bank touchpoints that each transaction must go through to be completed. However, recent changes to NACHA’s operating rules will make transfers faster than ever. As of September 2020, most, if not all, ACH transfers will be completed by the same day.

How To Make ACH Payments

VoPay connects directly to both ACH payments in the U.S. and EFT payments in Canada, allowing users to accept, send, and bulk transfer payments online. Our secure technology allows users to accept and manage ACH payments directly from any bank account.

ACH Payments in Canada

Digital payments in the U.S. are called ACH payments. In Canada, however, they are called EFT payments, or electronic transfer funds. The difference is that ACH payments go through the Automated Clearing House Network. For more information, read our in-depth blog post called Everything You Need to Know about EFT Banking.