Advanced ACH Payment Processing In Canada & The US

Connect to North America’s biggest bank account payment network using our dedicated Payment Portal and API integration.

Start processing ACH transfers with flat-rate transaction costs that let you push or pull ACH payments at scale.

See How Much You Could Save With Bank Account Payments:

Credit Card Cost

VoPay ACH Cost*

1.5%

3.5%

Credit Card Rate

Simplify ACH Payments with a Single API

VoPay’s ACH payment API lets you embed ACH processing into your products and services with ease.

Automated Payment Flows

Setup recurring billing for your customers to help save time, reduce errors and streamline your accounting process.

Fast Integration Times

Our developer-friendly API comes with simple SDKs to speed up integration time and reduce costs.

White-Label ACH Processing

Our ACH technology can be customized and embedded into any existing services or platforms.

Unlimited Virtual Wallets

Move money and segregate funds with confidence using VoPay’s Ledger Management technology.

Adaptive ACH Payment Flows for Unique Enterprise Use Cases

Elevate your payment processing with our robust ACH solution that empowers your business to handle transactions at any volume. Push and pull US bank account payments at scale with ease and utilize bulk payments and recurring transactions to simplify your payment processing.

ACH CREDIT

ACH DEBIT

BULK ACH PAYMENTS

WHITE-LABEL ACH

MULTIPLE ACH ACCOUNTS

Send money quickly and easily to users and service providers with direct bank payments.

Example: A gig platform makes payments to drivers, vendors and employees.

Send money quickly and easily to users and service providers with direct bank payments.

Example: A gig platform makes payments to drivers, vendors and employees.

Debit bank accounts instantly with complete visibility throughout the transaction life cycle.

Example: A lending platform automates payment collection from customers.

Debit, credit and reconcile ACH payments at large volumes with bulk batch processing.

Example: A subscription-based company collects payments from their customers.

White-label ACH processing lets you provide embedded payment flows in your own branding.

Example: A software company builds their own payment processing system into their SAAS platform.

Move funds between multiple ACH sub-accounts and keep funds segregated with independent ledgers.

Example: A law firm manages and holds funds in individual escrow accounts for its clients.

Same-Day ACH Payment Processing At Scale

Leverage VoPay’s direct link to the Same-Day ACH network to reliably process credit, debit and return transactions at multiple times throughout the day.

Automate bulk sending and collection of same-day payments using our API or Portal, and ensure time sensitive payments like payroll and claims are settled in the recipient’s account in 3 hours or less.

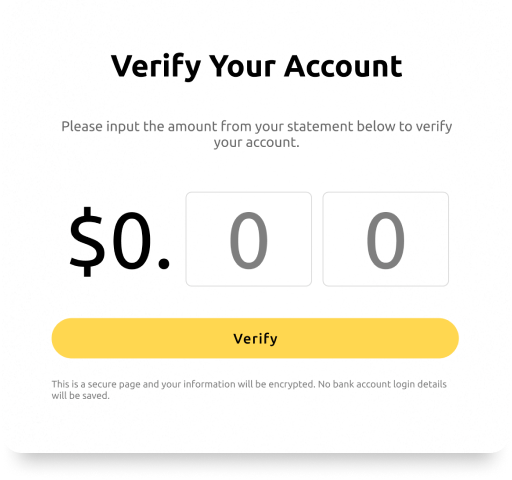

Connect Bank Accounts To Verify Validity & Ownership

Access VoPay’s risk reduction tools to stay compliant with Nacha network regulations and minimize your exposure to fraudulent activity.

Our bank account verification solution VoPay Verify enables customers to validate bank account ownership and functionality, meaning less chance of failed payments due to errors and fraud.

Connect Bank Accounts To Verify Validity & Ownership

Access VoPay’s risk reduction tools to stay compliant with Nacha network regulations and minimize your exposure to fraudulent activity.

Our bank account verification solution VoPay Verify enables customers to validate bank account ownership and functionality, meaning less chance of failed payments due to errors and fraud.

Use Multiple ACH Settlement Windows For Greater Control

Move money at any velocity with tailored ACH transaction times designed to work with your business requirements.

With VoPay you can send next-day ACH payments and even Same-Day ACH payments in addition to our standard ACH service.

ACH Payments For Any Industry

Our integration recipes are designed to give enterprises in any industry the tools to start processing ACH transactions as quickly as possible.

Faster earned wage access for workers to keep them loyal to your platform.

Low-cost deposits and collections to streamline your lending payments.

Handle large payments with ease and speed up cash-flow with faster payments.

Move money between US bank accounts with speed, efficiency and control.

Better recurring billing and reduced transaction fees for digital platforms.

Dedicated Payment Portal For ACH Transfers

Our user-friendly interface makes it easy to get started with ACH payment processing with a centralized view of your funds and transactions.

You can easily manage your transactions, view your account balances, access detailed reporting and analytics to gain valuable insights into user behavior.

Frequently Asked Questions

Speak to a Fintech Specialist Today!

Speak To Our Team

Speak to a Fintech Advisor to outline your needs and impact plan.

Access Sandbox

Start testing in the VoPay sandbox to explore our advanced API functions.

Sign & Onboard

Our compliance and onboarding team will guide you through the process.

Go Live!

Choose a production date and launch your integration with confidence!

Speak To Our Team

Speak to a Fintech Advisor to outline your needs and impact plan.

Access Sandbox

Start testing in the VoPay sandbox to explore our advanced API functions.

Sign & Onboard

Our compliance and onboarding team will guide you through the process.

Go Live!

Choose a production date and launch your integration with confidence!

Get to know the VoPay API

Get access to our developer friendly API and get a feel for how our payment solutions work.

Request a Call

Talk with our sales team

We are happy to answer your questions. Fill out the form and we will have one of our team members contact you.